")

Now part of

The Irish Government’s call to the Insurance industry to provide cover for properties located in high flood-risk areas in Ireland is a little surprising. Insurance is a promise of compensation for specific potential future losses in exchange for a periodic payment. The key word here is “potential”. Where the potential is so high that it can be replaced by “inevitable”, it’s not insurance any more – its charity.

So, the suggestion is that the insurance industry should provide charity to the unfortunate individuals who live in areas that will in the future be flooded and indeed be flooded with increased frequency. The justification for this demand, according to the Taoiseach, is the large profits that the industry makes and the view that they should be doing more. Fair enough.

But how did we get here? Planners and qualified professionals in local Government have for years known the areas that are prone to flooding and have in many cases warned against future impacts if development in flood-risk zones took place. In many cases, it was the elected representatives who forced through rezoning and permissions in unsuitable areas – including a certain Councillor McElvaney of Monaghan County Council as reported by Frank Mc Donald in the Irish Times in 2006.

But it hasn’t all been down to councillors. Many planners, under pressure to provide development land for expanding towns have allowed development in flood-zones. Even where flood risk is identified and prevention works stipulated in the conditions, either enforcement or design failings has resulted in the inevitable deluge and damage. Aldi in Ballybofey, for example, where permission was granted in 2013 subject to a requirements for embankments was under-water by December 2015.

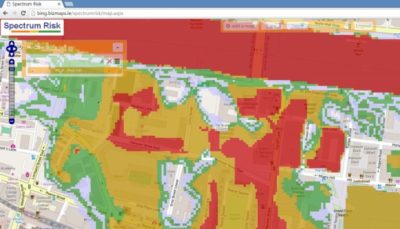

Location Intelligence technology is now developed in Ireland to a degree that insurance companies can tell quickly where a risk address is, and whether there are any significant environmental risks associated with the location. Flood risk models developed by private specialist companies such as JBA Risk and public models created by the OPW, can offer a fairly good prediction of the likely frequency (return period in years) and depth of flooding for any location in Ireland. Using accurate digital terrain and hydrological models, they can predict whether the floodwaters will come from rain, river or sea.

Add to this a fast and accurate address location engine (such as Autoaddress) and insurance companies can tell at quotation stage whether you live in a seasonal pond or on a hill. Often the name of the townland in the address can reveal local information which wiser generations have used, such as Pairc-na-big-flood-happens-here-all-the-time, Co Limerick. Historic Ordnance Survey maps also show floodplain areas known at the time, so in most cases the problem isn’t a dearth of information, just a lack of willingness to act on it.

If insurance companies can tell that an area is likely to flood and refuse cover – shouldn’t every planning department be required to consider the same information prior to rezoning or planning application decisions? If a decision is made to allow development on a known flood-risk area will the local authority compensate the unfortunate homeowners who buy a property there?

State-funded flood defence schemes are required nationwide but can only be justified in areas with sufficient assets to protect. The choice of barrier is also significant as some are permanent and others require human intervention to engage (demountable defences). Flash floods can catch out the latter and as a result, some flood models disregard them in identifying protected flood zone areas. This leaves the protected properties in a red flag category for insurance purposes. Even with an extensive flood defence programme, we are not going to protect all of the estimated 70,000 homes at risk of flooding (OPW estimate 2015)

Those living in flood zones deserve our sympathy as they are victims of poor planning and developer greed. A poll yesterday showed that 60% of policy holders (i.e. homeowners) surveyed in Ireland would not support increases in their premiums to finance the inevitable future claims coming from ill-conceived developments.

Whether the insurance industry adopt a white-knight role and covers the doomed is unknown. Some initial suggestions indicate that they would be willing to cover those defended by permanent barriers only.

If this problem has been caused by poor Government policy, misguided elected representatives and hungry developers shouldn’t compensation and guarantees come from the same source – i.e. developer levies and local government funds ?

And why are such easily identified flood zones being rezoned for development and granted permission on such a regular basis ?

Changes are coming – who’ll end up paying ?

@ 2016 Gamma.ie by Feargal O’Neill

About Gamma Location Intelligence

Gamma is a cloud-hosted solutions provider that integrates software, data and services to help our clients reduce risk through location intelligence. Established in Dublin, Ireland, in 1993, the company focuses heavily on leading-edge R&D including spatially aware AI and machine learning. Gamma has grown to become a market leader in the provision of location intelligence systems and services. Perilfinder™, Gamma’s risk mapping platform, is a cloud-hosted property-level risk assessment tool for sub-second assessment of environmental risk. Building on its market leading position across the island of Ireland, Perilfinder™ has recently extended its innovative platform to include the UK through partnerships with the major risk data providers.